ISSN: 1204-5357

ISSN: 1204-5357

Isaiah Onsarigo Miencha

Department of Banking and Finance, All Nations University, Ghana, Tel: +233200376654; Email: drimiencha@anuc.edu.gh

Murugesan Selvam

Department of Commerce and Financial Studies, Bharathidasan University, India

Seline Anne Onchangu

Department of Management Studies, Kisii University, Kenya

Visit for more related articles at Journal of Internet Banking and Commerce

Return on Assets; Banking; Large, Medium and Small

During the last decades, the banking sector experienced some transformation in its operating environment. Both external and domestic factors affected its structure and efficiency. Despite the increased trend towards banks disintermediation, observed in many countries, the role of banks in Kenya remains central in financing economic activity in general and different segments of the market in particular. A sound and profitable banking sector is better able to withstand negative shocks and contributes to the stability of the financial system [1]. Against this background, the present study attempts to examine the return on assets efficiency of sample Kenyan banks from large, medium and small size groups.

The Kenyan banking industry is now graduating beyond the traditional boundaries of plain vanilla banking. It has entered new areas such as wealth management, public banking, private banking, electronic banking, credit cards and investment advisory services. The sensible regulatory policies (framed by the Central Bank of Kenya) ensured that Kenyan banks emerged the safe from the global credit crisis. Kenya is one among the few countries, which have implemented Basel II framework.

However, the Kenyan banks are now facing a number of challenges such as frequent changes in technology required from modern banking, stringent prudential norms, increasing competition, worrying level of Non-Performing Assets (NPA), rising customer expectations, increasing pressure on profitability, asset liability management, liquidity and credit risk management, rising operating expenditure, shrinking spread etc. The reforms of Banking Sector have also brought the profitability under pressure. The efforts of Central Bank of Kenya to adopt international banking standards further, forced the banks to shift their focus to profitability for survival [2]. Hence, profitability has become the major area of concern for the management of the sample banks.

Therefore, the determinants of bank efficiency and profitability have attracted the interest of academic research as well as management of the banks, financial markets and bank supervisors.

Extensive research has been conducted on the banking sector in the global context. Some of them have worked on banking efficiency measurement. An attempt has been made in this paper to review the previous studies. The summarized results of reviews, relevant to this study, are given below.

Boris Vujcic and Igor Jemric [3] examined the efficiency of banks in transition using DEA-CRS and VRS. The inputs were interest and related costs, Commission, labor and capital while outputs were interest and related revenues and non-interest revenues. The result found that there was a problem for old as well as state owned banks as non-performing portfolios traced to previous system. Kosmidou [4] investigated the differences of profitability and efficiency between small and large Greek banks. The factors like profitability and operation (relating to the size of banks) were studied through a multi-criteria methodology. The study found that small banks seem to be more efficient and vulnerable. But large ones have lower operating costs due to the scale economies and their network. Ketkar [5] analyzed the efficiency and productivity of the Indian state controlled, nationalized, private and foreign banks. It was suggested that the Indian domestic banks need to greatly improve their efficiency through the introduction of computer technology, improved management skills and through the consolidation and mergers of banks.

Isik and Hassan [6] examined the commercial banks during the deregulation period. It was found that the Turkish private sector banks begun to close their gap with those public banks in the new environment. Shanmugam [7] studied efficiency of banks using stochastic frontier production function model. The study used four inputs variables (viz deposits, other borrowings, labor and fixed assets) and four output variables (viz net interest income, non-interest income, credits and investments) for analyzing the efficiency of sample banks. Wang, Huang and Yuan-Ze [8] employed nonparametric DEA methods to analyze the efficiency of commercial banks. According to CCR efficiency score analysis, two sample banks were relatively efficient. It to be noted that out of 16 commercial banks investigated in this study, two banks exhibited Constant Returns to Scale and seven banks exhibited Decreasing Returns to Scale. Kosmidou et al. [4] examined the performance of the small and large UK banks. It was found that small banks exhibited higher performance compared to large ones. It is significant that small UK-owned banks were profitable and recorded high capital ratios. Besides, the ratios of non-interest expenses/average assets, loan loss provisions/net interest revenue, interbank ratio, equity/total assets as well as equity/net loans contributed significantly in the discrimination between large and small banks.

Christian et al. [9] found that capital adequacy measured substantial information about a bank’s returns while a few of the individual variables represented asset quality. The size, growth and loan exposure measures did not appear to have any noteworthy explanatory power while examining the returns. The study also established that the change in total assets was a significant variable to be studied. Arabinda Saha [10] pointed out that the commercial banks like NCBs, PCBs, SCBs and FCBs have been playing a commendable role in achieving the economic growth of Bangladesh. The study focused the performance indicators of banking activities of Bangladesh. Isaiah Onsarigo Miencha [11] found that the private banks in Kenya performed well with better liquidity assets, compared to public banks and foreign banks.

The study found that banks have still a long way to go to sustain their competitive success. According to Prasad [12] there was efficiency among major commercial banks in India and most of the banks were satisfactorily efficient. The average performance of the banking sector ranged above 80 percent, which indicates the appropriate conversion of inputs into outputs. Isaiah et al. [13] analyzed the relative efficiency of sample commercial banks in Kenya. The relative average efficiency score by applying data envelopment analysis (BCC and CCR models) for all sample banks over the years was at 65.66 percent, which is fair. The study used two inputs (interest expense and non-interest expense) and two outputs (net interest income and non-interest income) for analysis. It was found that the extent of TE and SE varied across the ten sample commercial Kenyan banks over the study period. Isaiah Onsarigo Miencha et al. [14], measured efficiency of Kenyan commercial banks, using Data Envelopment Analysis. It is found that sample Kenyan commercial banks recorded volatility of variables during the study period.

The present study is unique because unlike others, an attempt has been made to study the efficiency of banks, in respect of return on assets, by using the BCC and CCR efficiency scores.

An attempt to study the efficiency in respect of return on assets of sample Kenya banks is important for benchmarking and strategic planning in the financial services sector. In Kenya, the dominance of the public sector has declined due to the use of technology and introduction of professional management by private and foreign sector banks that gained remarkable position in the Banking Industry. Private sector banks play an important role in the development of the Kenyan Economy. Many firms in the service industry, including the banks, face the problem of not producing better results in terms of return on assets efficiency. In particular, the last decade witnessed continuous changes in regulation, technology upgradation and competition in the global financial services industry and the Kenyan Commercial Banks are no exception to this. The efficiency of banks in general and technical efficiency in respect of return on assets in particular, has become an important issue in Kenya. It is therefore crucial to benchmark the efficiency of banks operating in Kenya, based on efficiency and hence this study on investigation of the efficiency (return on assets) of Kenyan Large, Medium and Small Bank groups.

Objectives of the Study

The main objective of this study was to analyze the Return on Assets of Kenyan Sample Banks

Hypothesis of the Study

The following null hypothesis was framed and tested in this study NH01: There is no significant difference in the efficiency of Return on Assets among the Kenyan Sample Banks.

There were 41 banks, including public and private sector, as on 31 March 2013. But it was found that the required data were available only for 35 banks. The final sample of 18 banks was selected by adopting the following criteria.

1. Fifty percent of the total banks for which the required data were available, were selected as the sample, (i.e 50% of 35=18 banks). These 18 banks were selected equally from large size, medium size and small size banks.

2. According to top index value, six banks from large size, (i.e. top 3 and lowest 3), six banks from medium size (top 3 and lowest 3) and six banks from small size (top 3 and lowest 3) were selected. The details of sample banks are given in Table 1.

| Bank Groups | Categories of Banks | SR. No. | Bank Names | Market Index Value as on 31 December 2013 | |

|---|---|---|---|---|---|

| Large size Banks | Top Size Banks | 1. | 1 | Kenya Commercial Bank Ltd | 12.83% |

| 2. | 2 | Standard Chartered Bank Ltd | 8.09% | ||

| 3. | 3 | Barclays Bank of Kenya Ltd | 7.65% | ||

| Lower Size Banks | 4. | 4 | Co-operative Bank of Kenya Ltd | 6.61% | |

| 5. | 5 | CFC Stanbic Bank Ltd | 5.43% | ||

| 6. | 6 | Equity Bank Ltd | 4.79% | ||

| Medium size Banks | Top Size Banks | 7. | 1 | Commercial Bank of Africa Ltd | 4.40% |

| 8. | 2 | Bank of India Ltd | 4.35% | ||

| 9. | 3 | Bank of Baroda Ltd | 4.23% | ||

| Lower Size Banks | 10. | 4 | National Industrial Development Bank of Kenya Ltd | 4.21% | |

| 11. | 5 | I & M Bank Ltd | 4.19% | ||

| 12. | 6 | Diamond Trust Bank (K) Ltd | 4.16% | ||

| Small size Banks | Top Size Banks | 13 | 1 | Habib Bank Ltd | 0.43% |

| 14 | 2 | Oriental Commercial Bank Ltd | 0.39% | ||

| 15. | 3 | Habib Bank A.G. Zurich | 0.37% | ||

| Lower Size Banks | 16. | 4 | Development Bank of Kenya Ltd | 0.33% | |

| 17. | 5 | Fidelity Commercial Bank Ltd | 0.27% | ||

| 18. | 6 | K-Rep Bank Ltd | 0.21% | ||

Source: Central Bank of Kenya Annual Report, 2013.

Table 1: Details of Sample Banks (Selected Based on Market Value as on 31/12/2013).

It is to be noted that for the purpose of analysis, the sample banks were classified as large, medium and small size study, as used by the Kenya Central Bank. The Kenya Central Bank used weighted composite index covering assets, deposits, capital, number of deposit accounts and loan accounts to classify the banks.

Sources of Data

The present study was mainly based upon secondary data. The required data were collected from annual report published by Central Bank of Kenya, various reputed journals and respective bank websites. The other relevant information for this study was collected from Books, News Papers, Magazines and Research Articles.

Period of Study

The study period covered a period of ten years from January 2004 to December 2013.

Tools Used

I. Data Envelopment Analysis (DEA) was used to analyze the efficiency in respect of return on assets of Kenyan sample banks.

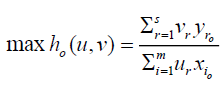

The weights for the ratio are determined by the restriction that similar ratios for every DMU have to be less than or equal to unity in respect of return on assets thus reducing multiple inputs and outputs to a single virtual output without requiring pre-assigned weights. Therefore, the efficiency score is a function of the weights of the virtual inputoutput combination. The efficiency score of a given DMUo is obtained by solving the following linear programming model.

Where

Xij=the amount of input i utilized by the jth DMU

Yrj=the amount of output r utilized by the jth DMU

Xi0=is the amount of ith input, and

Ui=weight given to input i

The linear programming model was run n times for identifying the efficiency scores of all the DMUs. Each DMU selects input weights that maximize its efficiency score. Generally, a DMU is considered to be efficient if it obtains a score of 1.00, implying 100 percent efficiency whereas a score of less than 1.00 implies that it is inefficient. Therefore, the mathematical programm problem for the ratio form by Charnes, Cooper and Rodhes. It is to be noted that the Technical Efficiency comprises pure technical efficiency and scale efficiency. This requires the estimation of the two DEA models – one with Constant Returns to Scale (CRS) and the other with Variable Returns to Scale (VRS). The model with constant returns to scale is known as the CCR Model. If there is difference in the two technical efficiency scores of a particular bank, it means that the bank’s scale is inefficient.

For the purpose of calculating data for this study, Data Envelopment Analysis Online Software (D.E.A.O.S) was used.

The present study suffers from the following major limitations.

• The study investigated the technical efficiency and inefficiency of Kenyan Commercial Banks in respect of return on assets and not their absolute efficiency.

• The three sample categories of banks (large, medium and small) were selected from public and private banks.

• The study was based only on secondary data and no primary data were used for this study.

• Limitations associated with the tools used, are applicable to this study.

• The period of the study was limited to ten years only.

The analysis of Return on Assets efficiency is divided into three, as given below.

Return on Assets Efficiency of Kenyan Commercial Banks (Top and Lower in the LARGE group) in respect of RETURN ON ASSETS

The results of technical efficiency for sample (top and lower in the large group) banks under CCR, BCC and Technical Efficiency models, during the study period from 2004 to 2013, are presented in Table 2.

| Sr. No. | I. Large – (top) banks in the large group | CCR | BCC | T.E |

|---|---|---|---|---|

| 1. | Kenya Commercial Bank Ltd | 0.890 | 0.924 | 0.907 |

| 2. | Standard Chartered Bank Ltd | 0.630 | 0.870 | 0.750 |

| 3. | Barclay's bank of Kenya Ltd | 1.000 | 1.000 | 1.000 |

| Average Score (among three top banks) | 0.840 | 0.931 | 0.886 | |

| II. Large – (lower) banks | ||||

| 4. | Co-operative Bank of Kenya Ltd | 0.323 | 0.665 | 0.544 |

| 5. | CFC Stanbic Bank of Kenya Ltd | 0.190 | 0.436 | 0.313 |

| 6. | Equity Bank Ltd | 1.000 | 1.000 | 1.000 |

| Average Score(among three lower banks) | 0.504 | 0.700 | 0.619 | |

| Average Score (overall among six sample banks) | 0.672 | 0.816 | 0.753 |

Source: www.centralbankofkenya.co.ke, Computed using DEA software online

Note: I) CCR – Charnes, Coopers and Rodhes Model, BCC – Bankers, Charnes and Rodhes, T.E – Technical Efficiency Models

II) Scale value of 1.000 indicates efficiency

III) Scale value of 0.500 to 0.999 indicates near or moderately efficiency

IV) Scale value of less than 0.499 indicates inefficiency of banks

Table 2: Results of Technical Efficiency Return on Assets (using CCR, BCC and T.E Models) for Kenyan Commercial Banks (three Top and three Lower banks in the Large group) during the study period from 2004 to 2013

Based on the results of inputs and outputs analysis under the CCR model, mean efficiency scores of 0.840 was earned by three top sample banks, 0.504 by three lower sample banks and 0.672 by all banks (top and lower large group), in respect of return on assets, during the study period from 2004 to 2013.

The analysis of the Table indicates that only two sample banks, namely, Barclays Bank of Kenya Ltd and Equity Bank Ltd recorded an efficiency score value of 1.00, for return on assets, during the study period, which indicates that these two sample banks utilized the return on asset effectively to find a place at the efficient frontier.

The Table clearly reveals that Kenya Commercial Bank Ltd and Standard Chartered Bank Ltd accounted for technical efficiency scores of 0.890 and 0.630 respectively during the study period and these two sample banks should use their inputs perfectly to earn a further score equal to 0.110 and 0.370 respectively, in respect of return on assets, to be at the efficient frontier. It is found that there was a high level of technical inefficiency in the case of Co-operative Bank of Kenya Ltd and CFC Stanbic Bank of Kenya, Ltd with return on assets score values of 0.323 and 0.190 respectively. These banks made poor use of inputs in the banking operation in Kenya during the study period. Hence these two banks should earn further scores of 0.677 and 0.810 respectively, in respect of return on assets. In short, these banks achieved a low level of growth in respect of return on asset during the study period from 2004 to 2013.

The detailed analysis of technical efficiency, under the BCC model, for sample banks is presented in Table 2. The average scores for return on assets, under the BCC model, were 0.931 by top three sample banks, 0.700 by three lower sample banks and 0.816 by all sample banks (average score) during the study period. The analysis indicates that only two sample banks, namely, Barclays Bank of Kenya Ltd and Equity Bank Ltd earned an efficiency score value of 1.000, in respect of return on assets during the study period. This reveals that these two sample banks maintained its inputs and outputs equations properly to be at the efficiency level of 1.000 in respect of return on assets. The other three sample banks namely, the Kenya Commercial Bank Ltd, Standard Chartered Bank Ltd and Co-operative Bank of Kenya Ltd recorded score values of 0.924, 0.870 and 0.665 respectively in respect of return on assets during the study period. Hence these three banks are required to earn further scores of 0.076, 0.130 and 0.335 respectively for return on assets to be at the efficiency frontier. But CFC Stanbic Bank of Kenya Ltd was relatively inefficient by earning return on assets score value of 0.436. In other words, CFC Stanbic Bank is required to earn a score by 0.564 by enhancing the return on assets to find place at the efficient frontier.

The analysis of Technical Efficiency model, as given at the Table 2 reveals that the Technical Efficiency values (average) of 0.886 were earned by three top sample banks, 0.619 by three lower sample banks and 0.753 by all sample banks (top large group and lower large group) in respect of Return on Assets during the study period. The analysis clearly shows that two sample banks, namely, Barclays Bank of Kenya Ltd and Equity Bank Ltd, earned an efficiency score value of 1.000 in respect of return on asset, during the study period, indicating the fact that these banks utilized the return on asset (input) effectively for the growth of the respective banks during the study period. But other sample banks, namely, the Kenya Commercial Bank Ltd, Standard Chartered Bank of Kenya Ltd and Co-operative Bank of Kenya Ltd earned score values of 0.907, 0.750 and 0.544 respectively in respect of return on asset which showed that the performance of all these sample banks were moderately efficient during the study period. Hence these three sample banks should exploit the existing inputs, to earn score values of 0.093, 0.250 and 0.456 respectively in respect of return on asset to be at the efficient level during the study period. It is surprising to note that CFC Stanbic Bank of Kenya Ltd earned an inefficient score value of 0.313 (low) and required to earn a score value of 0.687, by using its inputs efficiently, to be at the efficient frontier level. Only one sample bank, namely, CFC Stanbic Bank of Kenya Ltd was inefficient during the study period and hence it is suggested that such a bank could strengthen its performance by using their inputs intelligently to perform much better in terms of its outputs.

Chart 1 reveals the empirical results of Data Envelopment Analysis (DEA) to determine the efficiency of top and lower banks in the large group of Kenyan Commercial Banks, during the study period from 2004 to 2013. The Chart clearly shows that only two sample banks, namely, Barclays Bank of Kenya Ltd and Equity Bank Ltd were technically efficient by earning a score of 1.000, in respect of return on assets, throughout the study period. But Co-operative Bank of Kenya Ltd and CFC Stanbic Bank of Kenya Ltd earned an inefficiency score (i.e, less than one) during the study period. The efficiency level of other banks, namely, Kenya Commercial Bank Ltd and Standard Chartered Bank Ltd, was irregular but still efficient during the study period.

Chart 1: Technical Efficiency of RETURN ON ASSETS (Top and Lower) for Kenyan Commercial Banks under Large group during the study period (2004 to 2013).

Return on Assets Efficiency of Kenyan Commercial Banks (Top and Lower in the MEDIUM group) in respect of RETURN ON ASSETS

Table 3 displays the results of technical efficiency of sample banks (i.e three top and three lower banks in the medium group) in Kenya, estimated under CCR, BCC and Technical Efficiency models during the study period from 2004 to 2013. The Table illustrates that the mean efficiency scores, under the CCR model, were 0.524 (average) earned by three top large group sample banks, 0.816 by three lower sample group banks and 0.670 by overall top and lower bank groups during the study period.

| Sr. No. | I. Medium – (top) banks in the medium group | CCR | BCC | T.E |

|---|---|---|---|---|

| 1. | Bank of India | 0.209 | 0.355 | 0.282 |

| 2. | Bank of Baroda (K) Ltd | 0.363 | 0.611 | 0.487 |

| 3. | Commercial Bank of Africa Ltd | 1.000 | 1.000 | 1.000 |

| Average Score (among three top banks) | 0.524 | 0.655 | 0.590 | |

| II. Medium – (lower) banks | ||||

| 4. | National Industrial Development Bank of Kenya Ltd | 0.711 | 0.963 | 0.837 |

| 5. | I & M Bank Ltd | 1.000 | 1.000 | 1.000 |

| 6. | Diamond Trust Bank (K) Ltd | 0.738 | 0.988 | 0.863 |

| Average Score(among three lower banks) | 0.816 | 0.984 | 0.900 | |

| Average Score (overall among six sample banks) | 0.670 | 0.820 | 0.745 |

Source: www.centralbankofkenya.co.ke, Computed using DEA software online.

Note: I) CCR – Charnes, Coopers and Rodhes Model, BCC – Bankers, Charnes and Rodhes, T.E – Technical Efficiency Models

II) Scale value of 1.000 indicates efficiency

III) Scale value of 0.500 to 0.999 indicates near or moderately efficiency

IV) Scale value of less than 0.499 indicates inefficiency of banks

Table 3: Results of Technical Efficiency Return on Assets (using CCR, BCC and T.E Models) for Kenyan Commercial Banks (three Top and three Lower banks in the Medium group) during the study period from 2004 to 2013.

From the analysis of CCR model, it is clear that two sample banks, namely, Commercial Bank of Africa Ltd and I & M Bank Ltd accounted for a score value of 1.000, in respect of return on asset indicating that the resources (inputs) were perfectly utilized during the study period. The other sample banks, namely, National Industrial Development Bank of Kenya Ltd and Diamond Trust Bank (K) Ltd earned score values of 0.711 and 0.738 respectively by efficiently using asset of banks during the study period and these banks need to earn score values of 0.289 and 0.262 respectively to be at the efficient level. It is distressing to realize that Bank of India and Bank of Baroda (K) Ltd – (India based banks) were relatively inefficient and earned score values of 0.209 and 0.363 respectively, in respect of return on asset. Hence these two sample banks, namely, Bank of India and Bank of Baroda (K) Ltd should earn score values of 0.791 and 0.637 respectively, to be at the efficient level by initiating appropriate steps like introduction innovative banking products etc.

Table 3 also represents the average efficiency of score value, in respect of return on asset, under the BCC model. It is clear that the mean score value of 0.655 was earned by three top sample banks, 0.984 by three lower sample banks and 0.820 (overall average) by all sample banks. The Commercial Bank of Africa Ltd and I & M Bank Ltd were at the efficient frontier, with a score value of 1.000 in respect of return on asset during the study period. Other sample banks, namely, Bank of Baroda (K) Ltd, National Industrial Development Bank of Kenya Ltd and Diamond Trust Bank (K) Ltd earned score values of 0.611, 0.963 and 0.988 respectively for return on asset during the study period.

These three sample banks should earn score values of 0.389, 0.037 and 0.012 respectively, for return on asset, to be at the frontier level. The Bank of India earned a score value of 0.355 (less technical inefficiency score) and it is required to earn a score of 0.645 to be at the efficiency level.

The average return values, on asset efficiency, under the Technical Efficiency model, were 0.590 by three top sample banks, 0.900 by three lower sample banks and 0.745 (overall) by top and lower bank groups during the study period. These sample banks considered by this study performed at moderate and near efficient level during the study period from 2004 to 2013. Two other sample banks, namely, Commercial Bank of Africa Ltd and I & M Bank Ltd recorded an average score value of 1.000, in respect of return on asset, indicating their technical efficiency level to be at perfect level during the study period. Few other banks, namely, National Industrial Development Bank of Kenya Ltd and Diamond Trust Bank (K) Ltd earned score values of 0.837 and 0.863 respectively which were near efficient and hence these sample banks need to use inputs to earn scores equal to 0.163 and 0.137 respectively in respect of return on asset to be at efficient frontier. It is surprising to note that the Bank of India and Bank of Baroda (K) Ltd earned technical efficiency score values of 0.282 and 0.487 respectively, which was technically inefficient during the study period and hence these banks are required to earn scores of 0.718 and 0.513 respectively, by effectively using their assets to attain an efficient level of return. It is suggested that the Bank of India and Bank of Baroda (K) Ltd could extend their banking services to rural parts of Kenya and enhance their customer base and volume of transaction in Kenya. Besides, it would facilitate these banks to reap the benefits from large scale banking operations.

Chart 2 displays the overall efficiency level of three top as well as three lower sample banks in the medium group, in respect of return on assets. From the Chart, it is clear that Bank of India and Bank of Baroda (K) Ltd earned scores touching on inefficiency level whereas Commercial Bank of Africa Ltd and I & M Bank Ltd were at the efficiency level. Other sample banks, namely, National Industrial Development Bank of Kenya Ltd and Diamond Trust Bank (K) Ltd recorded fluctuations in the efficiency values (levels) which were near efficient during the study period.

Chart 2: Technical Efficiency of RETURN ON ASSETS (Top and Lower) for Kenyan Commercial Banks under Medium group during the study period (from 2004 to 2013).

Return on Assets Efficiency of Kenyan Commercial Banks (Top and Lower in the SMALL group) in respect of RETURN ON ASSET

The results of technical efficiency of sample (top and lower in the large group) commercial banks, under CCR, BCC and Technical Efficiency models, during the study period from 2004 to 2013, are presented in Table 4. It is clear that under the CCR model, the sample banks earned an average efficiency scores of 0.596 (top three sample banks), 0.816 (lower three sample banks) and 0.706 (an overall average efficiency score), in respect of return on assets, during the study period from 2004 to 2013. It is significant to note that two sample banks, namely, Habib Bank A. G. Zurich Ltd and Development Bank of Kenya Ltd were technically efficient by earning a score value of 1.000, in respect of return on asset, indicating that these banks perfectly utilized their return on asset (input) to earn high profits during the study period from 2004 to 2013. Besides, Habib Bank Ltd, Fidelity Commercial Bank Ltd and K- Rep Bank Ltd earned score values of 0.687, 0.653 and 0.795 respectively (in respect of return on asset) which was near efficient and these three sample banks had underutilized their assets during the study period. Therefore, the sample banks (Habib Bank Ltd, Fidelity Commercial Bank Ltd and K- Rep Bank Ltd) are required, to use the assets more intelligently, to produce the required level of outputs, to earn scores of 0.313, 0.347 and 0.205 respectively, for return on asset, to find places at the efficient level. It is surprising to note that there was inefficient use of assets (inputs) by Oriental Commercial Bank Ltd which earned an average score value of 0.101 in respect of return on asset and hence it needs to earn a score value of 0.899 to gain an efficient level.

| Sr. No. | I. Small – (top) banks in the small group | CCR | BCC | T.E |

|---|---|---|---|---|

| 1. | Habib Bank Ltd | 0.691 | 0.953 | 0.822 |

| 2. | Oriental Commercial Bank Ltd | 0.447 | 0.701 | 0.574 |

| 3. | Habib Bank A. G. Zurich Ltd | 1.000 | 1.000 | 1.000 |

| Average Score (among three top banks) | 0.713 | 0.885 | 0.799 | |

| II. Small – (lower) banks | ||||

| 4. | Development Bank of Kenya Ltd | 1.000 | 1.000 | 1.000 |

| 5. | Fidelity Commercial Bank Ltd | 0.435 | 0.681 | 0.558 |

| 6. | K-Rep Bank Ltd | 0.584 | 0.950 | 0.717 |

| Average Score(among three lower banks) | 0.673 | 0.877 | 0.758 | |

| Average Score (overall among six sample banks) | 0.693 | 0.881 | 0.779 |

Source: www.centralbankofkenya.co.ke, Computed using DEA software online

Note: I) CCR – Charnes, Coopers and Rodhes Model, BCC – Bankers, Charnes and Rodhes, T.E – Technical Efficiency Models

II) Scale value of 1.000 indicates efficiency

III) Scale value of 0.500 to 0.999 indicates near or moderately efficiency

IV) Scale value of less than 0.499 indicates inefficiency of banks

Table 4: Results of Technical Efficiency Return on Equity (using CCR, BCC and T.E Models) for Kenyan Commercial Banks (three Top and three Lower banks in the Small group) during the study period from 2004 to 2013.

The results under the BCC model are displayed at the Table, which shows an average return on asset efficiency score values of 0.738 (by top sample banks), 0.971 (by lower sample banks) and 0.855 by all banks during the study period from 2004 to 2013. From the analysis, it is clear that the performance of these banks, namely, the Habib Bank A. G. Zurich Ltd and Development Bank of Kenya Ltd was technically efficient. Two sample banks (the Habib Bank A. G. Zurich Ltd and Development Bank of Kenya Ltd) reported a higher average efficiency i.e, a score value of 1.000, in repect of return on asset, during the study period. The Habib Bank Ltd, Fidelity Commercial Bank Ltd and K- Rep Bank Ltd earned score values of 0.949, 0.915 and 0.997 respectively, is indicating that there was underutilization of total assets by these sample banks, which require values equal to 0.051, 0.085 and 0.003 respectively to be at the efficient level. It is unfortunate to note that Oriental Commercial Bank Ltd was technically inefficient, with a score value of 0.265, in respect of return on asset, indicating that there was inefficient use of assets by this bank and hence a further score equal to 0.735 is necessary to be at the efficient level.

According to the Technical Efficiency model, average values of sample banks, in respect of total assets, were 0.667 (by three top sample banks), 0.893 (by three lower sample banks), with an overall score value of 0.780 (by all sample banks), which reported to be near efficient. The return performance of some sample banks (namely, Habib Bank A. G. Zurich Ltd and Development Bank of Kenya Ltd) was technically efficient, with a score of 1.000, during the study period. The few sample banks (namely Habib Bank Ltd, Fidelity Commercial Bank Ltd and K – Rep Bank Ltd) earned an efficiency scores of 0.818, 0.784 and 0.896 respectively and these sample banks needed score values of 0.182, 0.216 and 0.104 respectively to be at the efficient level, during the study period from 2004 to 2013. It is unfortunate that Oriental Commercial Bank Ltd earned a score of 0.183 resulting from inefficient in using its assets during the study period and this bank requires a further score of 0.817 to find a place at the efficient level. From the analysis of Table and feedback, the bank officials of bank are advised to maintain a good rapport with the customers in such a way to develop a social banking environment and increase the outputs (return) by exploiting to the full the available assets.

Chart 3: Technical Efficiency of RETURN ON EQUITY (Top and Lower) for Kenyan Commercial Banks under Small group during the study period (from 2004 to 2013).

Chart 3 displays the results of technical efficiency of sample banks, in respect of return on assets. The sample banks, namely, Habib Bank A. G. Zurich Ltd and Development Bank of Kenya Ltd showed a positive return on assets efficiency level under the CCR, BCC and Technical efficiency models. There was variance in the values of technical efficiency (i.e, with a decrease and increase) in respect of sample banks like Habib Bank Ltd, Fidelity Commercial Bank Ltd and K-Rep Bank Ltd, under CCR, BCC and Technical efficiency models. There was inefficiency registered by Oriental Commercial Bank Ltd under CCR, BCC and Technical efficiency models, in respect of return on assets, during the study period.

The present study investigated the efficiency (Return on Assets) of large, medium and small size group of sample banks in Kenya, using the data envelopment analysis. The result of this study indicates the fragility in the Kenyan sample banks during the study period. In other words, the efficiency level of various sample banks varied from time to time, with volatility in the scores. None of the segment of bank groups was uniform throughout the study period. Comparative study of the financial efficiency was more useful to strengthen the financial variables by the management of these bank groups. Commercial Bank of Africa Ltd and Habib Bank A. G. Zurich Ltd recorded high efficiency scores while Bank of India and Bank of Baroda (K) Ltd earned the least score value in respect of return on assets during the study period. This means that the variation of the efficiency level of banks was caused by the failure in management of sample banks in the use of their assets. The efficiency of Kenyan banks should be improved, by interacting with people, particularly for explaining to them banking products and services. Bankers must prioritize economic development of people in Kenya rather than profits for banks. This would lead the people to access banking services to the maximum, particularly in rural areas where people still feel that the commercial banks are just another form of organized moneylenders. All round efforts are to be made by Kenyan banks to create confidence among people about banking services. At the same time, efficient banks need to be particular about maintaining their efficiency level in future too while weak banks need to initiate all efforts to improve their efficiency level by effectively using this assets.

The following are pointers towards further research.

1. A study could be made with other variables like Net Interest Income, Net Profit Margin, Non-Performing Loans, Interest Spread, Capital Adequacy Ratio and Yield on Earning Assets

2. A study, with similar objectives, could be made from time to time.

3. A comparative study can be made within the region and other foreign countries.

4. Similar study could be made from the perspective of customers and bankers.

Copyright © 2025 Research and Reviews, All Rights Reserved